It’s always tough teaching intro level courses. You must sacrifice some subtlety for clarity and you can’t get too deep in the weeds. That’s fine sometimes because simple economics is not necessarily simple-minded economics. However, there are important topics that are left on the cutting room floor. For example, this fall I have used our Competitive Market game to teach over a thousand undergraduates about supply and demand. There were buyers with diminishing marginal utility and sellers with increasing marginal costs. When trade occurred in a double oral auction the markets converged to equilibrium. In the first round prices are sporadic and quantity traded is much less than the equilibrium prediction. Buyers offer stingy bids and sellers hold out for higher prices. Across rounds both realize this is not a good strategy for earning profits. By the third round convergence happens pretty swiftly.

In the first round prices are sporadic and quantity traded is much less than the equilibrium prediction. Buyers offer stingy bids and sellers hold out for higher prices. Across rounds both realize this is not a good strategy for earning profits. By the third round convergence happens pretty swiftly. But suppose the trading institution were still a double oral auction but we made three changes: (1) Allowed students to be both buyers and sellers, (2) We made their stock of goods storable across rounds, and (3) Their stock of goods paid out a dividend at the end of each round. What would happen? The answer seems to be: Bubbles and Crashes.

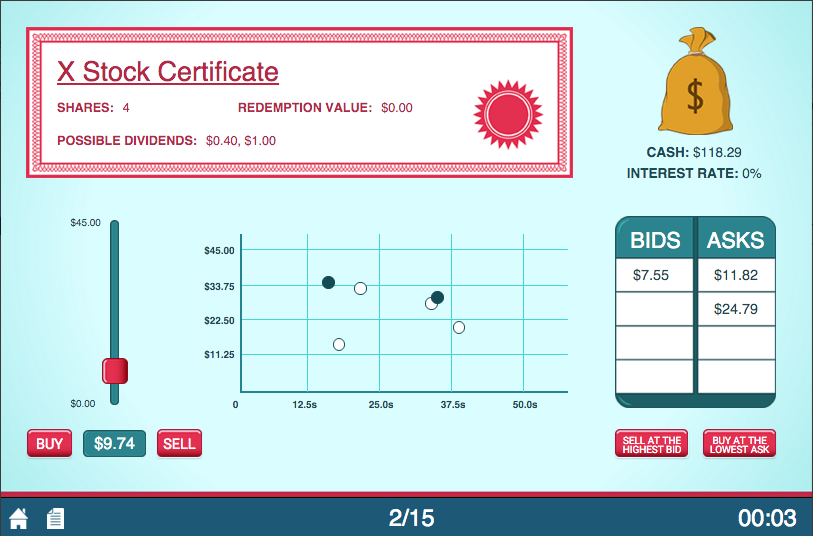

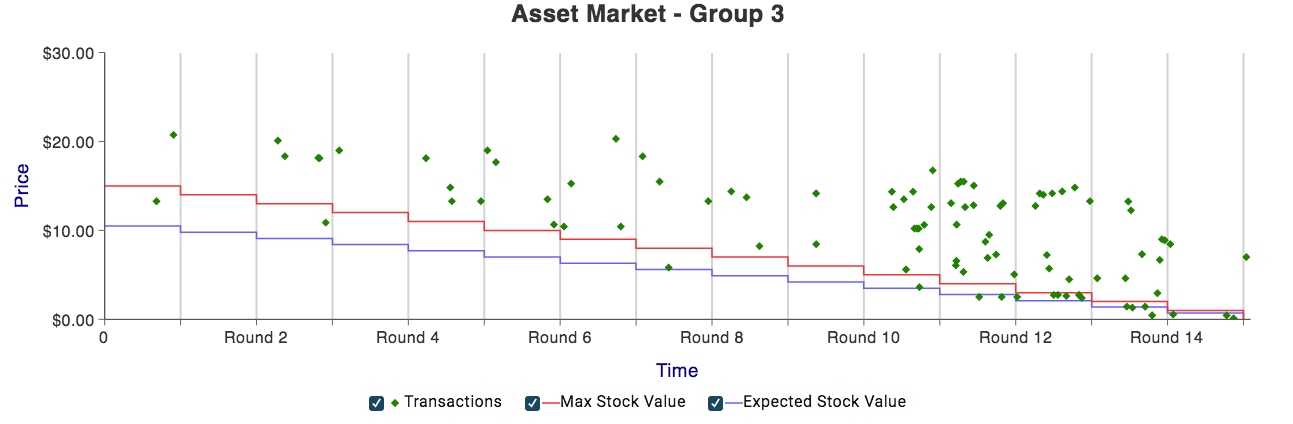

But suppose the trading institution were still a double oral auction but we made three changes: (1) Allowed students to be both buyers and sellers, (2) We made their stock of goods storable across rounds, and (3) Their stock of goods paid out a dividend at the end of each round. What would happen? The answer seems to be: Bubbles and Crashes. Let’s look at our Asset Market game. The default parameters of that game have students buying and selling shares of stock in groups of 10 across 15 rounds. With the default parameters the stocks have zero redemption value after trade concludes in the 15th round. The value of a stock is based on its expected flow of dividends. At the conclusion of each round there is a 50-50 chance the dividend per stock is 40 cents or $1. With a redemption value of zero the stock has a declining expected value towards zero. The blue line shows the expected value. The red line shows what the most optimistic outcome would be (if you received a $1 per stock each round for all the remaining rounds).Despite the everywhere decreasing expected value the transaction prices for these stocks can become quite large and then towards the 15th round, when students see the writing on the wall, the prices crash down to the intertemporal competitive equilibrium. In other words, prices in this environment DO reach equilibrium eventually, but not until the bubble has burst.

Let’s look at our Asset Market game. The default parameters of that game have students buying and selling shares of stock in groups of 10 across 15 rounds. With the default parameters the stocks have zero redemption value after trade concludes in the 15th round. The value of a stock is based on its expected flow of dividends. At the conclusion of each round there is a 50-50 chance the dividend per stock is 40 cents or $1. With a redemption value of zero the stock has a declining expected value towards zero. The blue line shows the expected value. The red line shows what the most optimistic outcome would be (if you received a $1 per stock each round for all the remaining rounds).Despite the everywhere decreasing expected value the transaction prices for these stocks can become quite large and then towards the 15th round, when students see the writing on the wall, the prices crash down to the intertemporal competitive equilibrium. In other words, prices in this environment DO reach equilibrium eventually, but not until the bubble has burst. When one takes a step back the finding of bubbles is remarkable. Although there are historical examples like "tulipmania," the south sea bubble, and more recent experiences with the tech and housing bubbles it is hard to refute the claim that those prices weren't "right." However, in these games you can show clearly how price deviates from fundamental value. In this game prices often soar to heights even the most optimistic traders should not want to pay. This brings up an important question: Why does convergence happen so quickly in the competitive market but in the asset market there is so much froth in the transaction prices? (I will provide at least one explanation in an upcoming blog post)Besides demonstrating that bubbles are real and can happen, what else can you use this game to teach students about? Students can learn about factors that attenuate bubbles. One of the most robust results is that experience reduces the formation of speculative bubbles. In addition to these learning objectives the game also provides a platform for teaching about asset pricing. After two iterations of the game your students will have built up some intuition about the nuts and bolts of asset pricing. Ask them, “How did you figure out what you should buy the asset at?” They’ll likely talk about the possible dividend outcomes, the probability of those outcomes happening, and the number of periods left in trading. Take it from there.

When one takes a step back the finding of bubbles is remarkable. Although there are historical examples like "tulipmania," the south sea bubble, and more recent experiences with the tech and housing bubbles it is hard to refute the claim that those prices weren't "right." However, in these games you can show clearly how price deviates from fundamental value. In this game prices often soar to heights even the most optimistic traders should not want to pay. This brings up an important question: Why does convergence happen so quickly in the competitive market but in the asset market there is so much froth in the transaction prices? (I will provide at least one explanation in an upcoming blog post)Besides demonstrating that bubbles are real and can happen, what else can you use this game to teach students about? Students can learn about factors that attenuate bubbles. One of the most robust results is that experience reduces the formation of speculative bubbles. In addition to these learning objectives the game also provides a platform for teaching about asset pricing. After two iterations of the game your students will have built up some intuition about the nuts and bolts of asset pricing. Ask them, “How did you figure out what you should buy the asset at?” They’ll likely talk about the possible dividend outcomes, the probability of those outcomes happening, and the number of periods left in trading. Take it from there.

In the first round prices are sporadic and quantity traded is much less than the equilibrium prediction. Buyers offer stingy bids and sellers hold out for higher prices. Across rounds both realize this is not a good strategy for earning profits. By the third round convergence happens pretty swiftly. But suppose the trading institution were still a double oral auction but we made three changes: (1) Allowed students to be both buyers and sellers, (2) We made their stock of goods storable across rounds, and (3) Their stock of goods paid out a dividend at the end of each round. What would happen? The answer seems to be: Bubbles and Crashes.Let’s look at our Asset Market game. The default parameters of that game have students buying and selling shares of stock in groups of 10 across 15 rounds. With the default parameters the stocks have zero redemption value after trade concludes in the 15th round. The value of a stock is based on its expected flow of dividends. At the conclusion of each round there is a 50-50 chance the dividend per stock is 40 cents or $1. With a redemption value of zero the stock has a declining expected value towards zero. The blue line shows the expected value. The red line shows what the most optimistic outcome would be (if you received a $1 per stock each round for all the remaining rounds).Despite the everywhere decreasing expected value the transaction prices for these stocks can become quite large and then towards the 15th round, when students see the writing on the wall, the prices crash down to the intertemporal competitive equilibrium. In other words, prices in this environment DO reach equilibrium eventually, but not until the bubble has burst.When one takes a step back the finding of bubbles is remarkable. Although there are historical examples like "tulipmania," the south sea bubble, and more recent experiences with the tech and housing bubbles it is hard to refute the claim that those prices weren't "right." However, in these games you can show clearly how price deviates from fundamental value. In this game prices often soar to heights even the most optimistic traders should not want to pay. This brings up an important question: Why does convergence happen so quickly in the competitive market but in the asset market there is so much froth in the transaction prices? (I will provide at least one explanation in an upcoming blog post)Besides demonstrating that bubbles are real and can happen, what else can you use this game to teach students about? Students can learn about factors that attenuate bubbles. One of the most robust results is that experience reduces the formation of speculative bubbles. In addition to these learning objectives the game also provides a platform for teaching about asset pricing. After two iterations of the game your students will have built up some intuition about the nuts and bolts of asset pricing. Ask them, “How did you figure out what you should buy the asset at?” They’ll likely talk about the possible dividend outcomes, the probability of those outcomes happening, and the number of periods left in trading. Take it from there.